In a Harvard Business Review blog post, author Mark Bonchek discusses the need to change people’s mental models to embrace new innovative offerings. It’s a compelling view on how to increase adoption for the new or never-before-seen, and the author shares some good examples of this shift with Salesforce.com’s Software as a Service and Apple’s products. But it’s no easy task changing how your customers view things and not all innovation demands a shift in customers’ mental models to be successful.

After all, a Steve Jobs is rare and many mental shifts require cultural and industry-wide efforts outside a single company’s control. Take the example of Salesforce.com, a model of SaaS, but hardly the only one. A key adopter of SaaS as a commercial concept was Oracle’s Larry Ellison, who was a few years ahead of his time. Things like faster bandwidth and the collective move of the industry led to broader acceptance, something years in the making and that couldn’t have occurred purely through a single player.

At Continuum, we see the need to shift a customer mental model, but only if the existing one is unable to meet business and customer needs. When we partnered with Procter & Gamble on rethinking the floor-cleaning experience, the mop-and-bucket solution was broken for both the business model and user needs, requiring us to design a new approach and get people to adopt the new behaviors associated with it. And that was a major reason why the Swiffer achieved the success it did.

But often, the most effective and efficient way to engage and drive adoption of new offerings is to fit within existing mental models. It asks more of the organization but less of customers. And guess which one you have more control over? Beginning with a deep understanding of your customers and their existing worldviews, and then designing your solutions to best fit within those, is easier and lowers barriers to adoption.

The pressing issue we see for many companies these days is shifting to a customer-centered approach in solving problems and delivering value. Their processes, structures, offerings, and channels are often built for their benefit, and within their mental model, not customers’. And so companies are frequently requiring their customers to change, often with poor results.

The financial services industry is a perfect example. Health and life insurance companies ask you to think about potential negative ‘what if’ scenarios and plan for their impact today. They ask you to select from products with names like “disability insurance,” have you understand deductibles and elimination periods, and send for your review an explanation of benefits (which, they remind you on the piece of paper in bold type, is not a bill). Banks are no better with their complex products and confusing planning tools in the form of charts and graphs.

Before assuming that you need to apply some ‘mind design’ to your customers, look at how you might better design your products and services to fit them.

Simple Bank, recently acquired by BBVA, focused on Gen Y and their desire to be financially responsible while enjoying what money they do have accessible. Simple’s digital solution lets people set aside money to pay bills, create savings goals, and automate contributions, and then easily communicates the dollar amount left. A friend calls up to see if you want to go to dinner? Just check the Simple app and you can make a quick decision on what’s safe to spend after bills and savings. The name of the feature? It’s called, um, “Safe to Spend.” No math. No charts. No future-scenario guesswork.

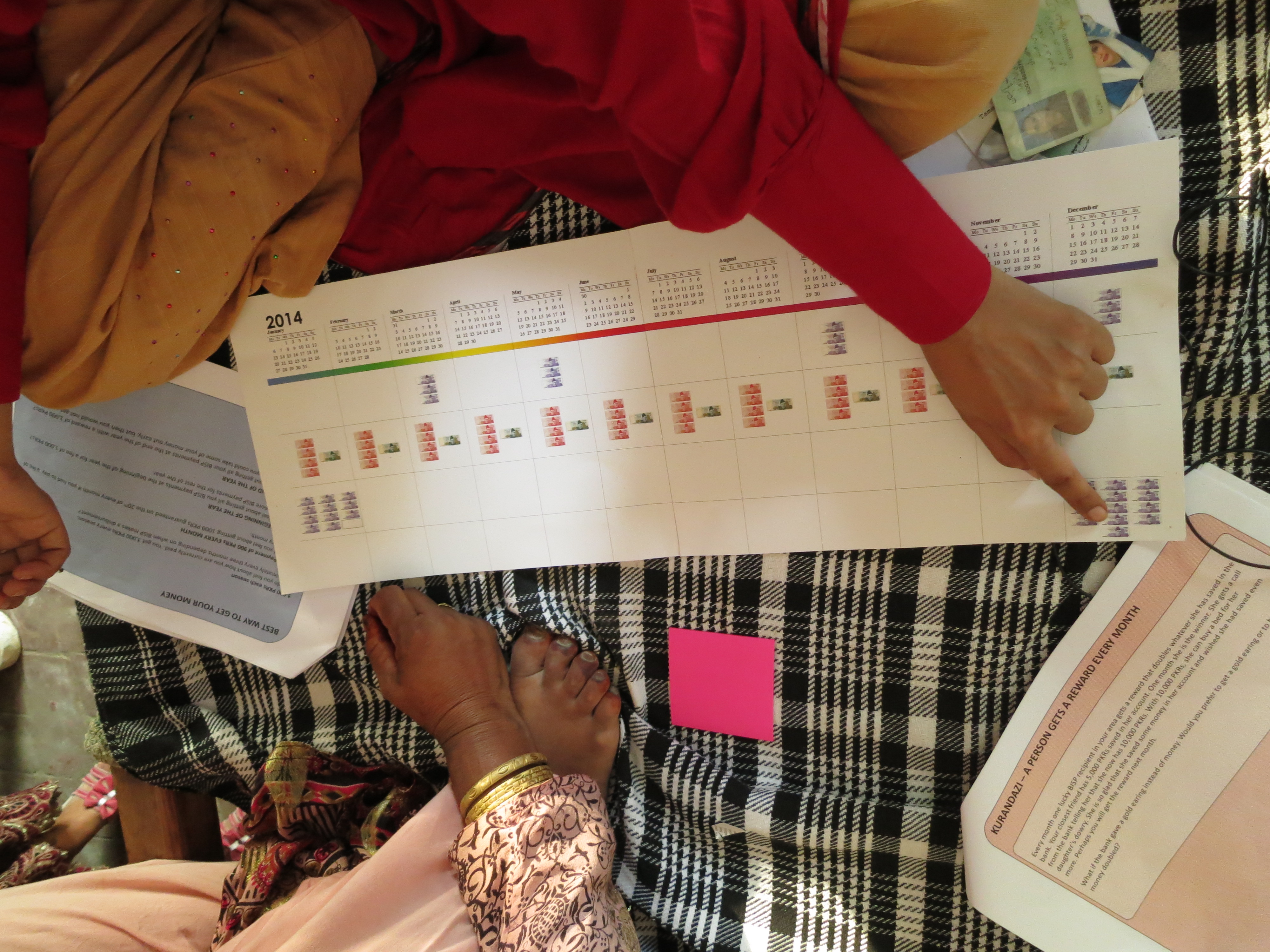

The World Bank’s Consultative Group to Assist the Poor (CGAP) and Habib Bank Limited worked with Continuum to identify new product opportunities that better serve poor women in Pakistan. A team spent weeks in the field interviewing and understanding the financial needs and limitations of these women.

Most are illiterate, and though they are financially savvy in their context, they lacked any positive experience with banks. The team found that bank-centric ideas like a loan or savings were abstract concepts.

Despite the women valuing the targeted behavior (many were consistently saving for a dowry for their daughters), the gap between the bank’s communication and that of the women kept them from being customers. The solutions involved literal pictures instead of words or abstract concepts, and products understandable and usable to them anchored in their mental models. Not a bank’s.Communicating Savingsandloans

Both of these organizations took time to understand how their customers see the world and then adapted their offerings accordingly.

As with the iPhone or the Swiffer, driving a shift in mental models is a valid approach. But it shouldn’t be the default. There are many new and innovative ideas unable to overcome the enormous hurdle that is changing a customer’s way of thinking. Even the most technologically-clever, well-funded, and well-publicized efforts may not always move people— although the Segway does still move tourists through major cities around the world.

If you want to increase your odds of success, you have to understand your customers and then meet them more than halfway, rather than count on successfully dragging them along with you. Rather than fighting customers with every new innovative offering, first look at if you can embrace how they see things and fit what you do to how they already think.

About the Author

Jon CampbellHead of Experience & Service Design

Jon CampbellHead of Experience & Service DesignJon helps organizations become customer-centered and develop their internal capability for repeatedly creating, launching, and scaling new offerings and compelling customer experiences.

Prior to EPAM Continuum, Jon served as Manager, Prospect Marketing, at Harley-Davidson Motor Co., overseeing lead generation, lead nurturing, and interactive programs focused on the acquisition of new customers and development of compelling customer journeys. He also spent time at ad agency Cramer-Krasselt, working on brand strategy, marketing communications, and new product development.

Jon holds a master of design methods degree from Chicago’s Institute of Design (IIT) and a BA in journalism from the University of Wisconsin.

More from Jon Campbell